Engineer, Manage Thyself

The course of my side projects often follows a pattern. I begin with enthusiasm, writing code based on little more than a picture in my mind. One, two, three days of manic productivity later, I may have written thousands of lines of code, but the enthusiasm is spent. I look around at what I’ve built, and all I can see is how far away from “finished” it is. I feel discouraged, and I feel unskilled. The stack of tasks to do has increased, not decreased, and I have no guidance on what to do next.

It’s at this point that I remember I’ve learned this lesson before. The lesson is: all non-trivial projects need management. Even when its a team of one.

While we are conditioned to think of management as a role, I think it is more useful to think of it as an activity. We could define this activity negatively as "everything that isn't building". Positively, it’s the actions of planning, decision making, allocating resources, reflecting, and adjusting. Far from something done only by "managers", this activity actually takes place to differing extents in almost every role in an organization. It happens whenever we are sitting in the frontal lobe, thinking about the project from the outside vantage point, and constructing a theory that connects the present moment to a future one where the project is completed.

So how do we manage ourselves?

The first thing to do is to carve out time for management tasks. Don’t assume that it will just happen. As engineers, we usually feel the best when we are coding. If we follow what feels good, we may never remove ourself from our IDEs. Therefore its best to actually put time on your own calendar to manage yourself. I have always found a basic weekly sprint to feel very familiar so I will often use that template. Weekly planning/retro on Monday. Daily “standup”’s. As a solo person, a “standup” can be as simple as reviewing what you did yesterday, and setting goals for today.

Second is to make a plan.

- what does “finished” mean?

- what are are the constituent components of the finished project?

- for each component, recursively, what is the plan?

- how long will I spend on each part?

The third is to work to the plan.

The fourth is to reflect and update the plan as necessary.

Managing ourselves is a great way to ultimately get more done when we are working alone. The best part is, managing yourself well will actually improve your ability to work with others. It will even improve your ability to manage others. Many of the skills of high performing ICs are really management skills: estimation, planning, and communication. Managing yourself is a great way to be a better IC.

The course of my side projects often follows a pattern. I begin with enthusiasm, writing code based on little more than a picture in my mind. One, two, three days of manic productivity later, I may have written thousands of lines of code, but the enthusiasm is spent. I look around at what I’ve built, and all I can see is how far away from “finished” it is. I feel discouraged, and I feel unskilled. The stack of tasks to do has increased, not decreased, and I have no guidance on what to do next.

It’s at this point that I remember I’ve learned this lesson before. The lesson is: all non-trivial projects need management. Even when its a team of one.

While we are conditioned to think of management as a role, I think it is more useful to think of it as an activity. We could define this activity negatively as "everything that isn't building". Positively, it’s the actions of planning, decision making, allocating resources, reflecting, and adjusting. Far from something done only by "managers", this activity actually takes place to differing extents in almost every role in an organization. It happens whenever we are sitting in the frontal lobe, thinking about the project from the outside vantage point, and constructing a theory that connects the present moment to a future one where the project is completed.

So how do we manage ourselves?

The first thing to do is to carve out time for management tasks. Don’t assume that it will just happen. As engineers, we usually feel the best when we are coding. If we follow what feels good, we may never remove ourself from our IDEs. Therefore its best to actually put time on your own calendar to manage yourself. I have always found a basic weekly sprint to feel very familiar so I will often use that template. Weekly planning/retro on Monday. Daily “standup”’s. As a solo person, a “standup” can be as simple as reviewing what you did yesterday, and setting goals for today.

Second is to make a plan.

- what does “finished” mean?

- what are are the constituent components of the finished project?

- for each component, recursively, what is the plan?

- how long will I spend on each part?

The third is to work to the plan.

The fourth is to reflect and update the plan as necessary.

Managing ourselves is a great way to ultimately get more done when we are working alone. The best part is, managing yourself well will actually improve your ability to work with others. It will even improve your ability to manage others. Many of the skills of high performing ICs are really management skills: estimation, planning, and communication. Managing yourself is a great way to be a better IC.

How to feel when your startup feels easy

I did something hard once: I took my startup from zero to $1m in daily volume in 4 months. Something has bothered me ever since: it felt easy.

That summer, my team had pivoted and set a new challenge for ourselves: start a crypto market making business and grow it from zero to 10% of all trading volume in three months. We didn’t know how to do this, but we had an idea for a simple trading bot and strategy that would get us started. When we turned this bot on for the first time, I watched it work for an hour before I turned to my cofounder and said “We are 2% of all trading in this market”. Our first guess had gotten us 20% of the way there! With a few more straightforward improvements, we hit and surpassed our goal with time to spare. With success came attention, and chatter that we were one of the “hot” companies in our YC batch. When it came time to raise our seed round, we were able to pull in 7 figures with only a few days of meetings.

If you’re a founder, and are feeling your jaw tighten as I tell you how easy my startup was, don’t worry. This “easy” period was a brief interlude in years of struggle. Hard was so familiar, that the departure from it actually felt distressing. Startups are hard, right? So why did this feel easy?

Maybe we were frauds. We were doing something easy and letting people believe that it was hard, or at least, not correcting them when they were impressed. I worried that if people really knew how easy this was, they’d laugh, and lose interest in us right away.

It’s obvious to me today that this idea was wrong. Instead, I’ve come to believe that ease is a critical ingredient in startups.

Let’s deal first with the imposter syndrome. I had internalized — through culture and personal experience — that startups are hard, and mutated this into the notion that everything about startups should be hard, all the time. This was a mistake.

No one ever said that every day of your startup has to be hard. The first phase of a startup is a search for something people want. The search is often very hard. This doesn’t mean that the thing that you find will be hard to build or sell. Once you find something people want, that part of your project will get easier in a step wise way. The ease is a signal that you’re doing something something right!

For a certain class of idea, the perception that it is hard may actually make it easy. In our case, I can say with hindsight that we — and many other people — overestimated how sophisticated crypto markets were in that era. If more people thought this was easy, there would have been more competition in the markets, and it would have been hard. Because it sounded hard, few people wanted to do it, and our simple approaches were very successful. The trick was that you had to be willing to do something that sounded hard in order to discover that it was easy.

This idea that there is a delta between perceived and realized difficulty of a project may be one reason why startups exist at all. If everything was equally easy and hard as it appeared, then resources would already be perfectly allocated. There would be no edge for small teams to discover.

It’s worthwhile to consider this delta from the opposite direction. I’ve been speaking about what it feels like from the inside, when you’re doing something hard that feels easy, but what does this feel like from the perspective of an outside observer? I think we all know. You see someone achieve something hard, you feel a sense of awe, and possibly a pang of insecurity: the fear that you’ll never be as good as that person.

This makes me suspect that part of my discomfort with ease was because of ego. I wanted to feel the same way about myself that I felt about the people I admired. The people I admired did things that looked very hard, so — in a perverse way — I wanted what I was doing to feel hard. Doing something easy didn’t give me the self-satisfaction I was searching for.

This is an emotional logic that we should all be happy to let go of. Finding something that feels easy, even for a few months, in the midst of a startup grind is a gift. The people we admired were never afraid to take an easy win when it presented itself.

So don’t worry if your startup suddenly starts to feel easy, that probably means you’re doing something right. When you see other people do hard things, don’t take it as evidence that they are better than you, rather, take it as proof that hard things can actually be done.

Most importantly, consider: maybe the hard thing you’ve been thinking of is easier than you think.

I did something hard once: I took my startup from zero to $1m in daily volume in 4 months. Something has bothered me ever since: it felt easy.

That summer, my team had pivoted and set a new challenge for ourselves: start a crypto market making business and grow it from zero to 10% of all trading volume in three months. We didn’t know how to do this, but we had an idea for a simple trading bot and strategy that would get us started. When we turned this bot on for the first time, I watched it work for an hour before I turned to my cofounder and said “We are 2% of all trading in this market”. Our first guess had gotten us 20% of the way there! With a few more straightforward improvements, we hit and surpassed our goal with time to spare. With success came attention, and chatter that we were one of the “hot” companies in our YC batch. When it came time to raise our seed round, we were able to pull in 7 figures with only a few days of meetings.

If you’re a founder, and are feeling your jaw tighten as I tell you how easy my startup was, don’t worry. This “easy” period was a brief interlude in years of struggle. Hard was so familiar, that the departure from it actually felt distressing. Startups are hard, right? So why did this feel easy?

Maybe we were frauds. We were doing something easy and letting people believe that it was hard, or at least, not correcting them when they were impressed. I worried that if people really knew how easy this was, they’d laugh, and lose interest in us right away.

It’s obvious to me today that this idea was wrong. Instead, I’ve come to believe that ease is a critical ingredient in startups.

Let’s deal first with the imposter syndrome. I had internalized — through culture and personal experience — that startups are hard, and mutated this into the notion that everything about startups should be hard, all the time. This was a mistake.

No one ever said that every day of your startup has to be hard. The first phase of a startup is a search for something people want. The search is often very hard. This doesn’t mean that the thing that you find will be hard to build or sell. Once you find something people want, that part of your project will get easier in a step wise way. The ease is a signal that you’re doing something something right!

For a certain class of idea, the perception that it is hard may actually make it easy. In our case, I can say with hindsight that we — and many other people — overestimated how sophisticated crypto markets were in that era. If more people thought this was easy, there would have been more competition in the markets, and it would have been hard. Because it sounded hard, few people wanted to do it, and our simple approaches were very successful. The trick was that you had to be willing to do something that sounded hard in order to discover that it was easy.

This idea that there is a delta between perceived and realized difficulty of a project may be one reason why startups exist at all. If everything was equally easy and hard as it appeared, then resources would already be perfectly allocated. There would be no edge for small teams to discover.

It’s worthwhile to consider this delta from the opposite direction. I’ve been speaking about what it feels like from the inside, when you’re doing something hard that feels easy, but what does this feel like from the perspective of an outside observer? I think we all know. You see someone achieve something hard, you feel a sense of awe, and possibly a pang of insecurity: the fear that you’ll never be as good as that person.

This makes me suspect that part of my discomfort with ease was because of ego. I wanted to feel the same way about myself that I felt about the people I admired. The people I admired did things that looked very hard, so — in a perverse way — I wanted what I was doing to feel hard. Doing something easy didn’t give me the self-satisfaction I was searching for.

This is an emotional logic that we should all be happy to let go of. Finding something that feels easy, even for a few months, in the midst of a startup grind is a gift. The people we admired were never afraid to take an easy win when it presented itself.

So don’t worry if your startup suddenly starts to feel easy, that probably means you’re doing something right. When you see other people do hard things, don’t take it as evidence that they are better than you, rather, take it as proof that hard things can actually be done.

Most importantly, consider: maybe the hard thing you’ve been thinking of is easier than you think.

How we survived 5 years in the most dangerous market in the world

The goal of Tinker was to build the Goldman Sachs of the blockchain-future, and our thesis was good. Granting that cryptocurrencies would be the next medium of finance, we’d start out with an early lead in market making, use that edge to expand into other investment products as the market grew, and by the time the traditional investment banks caught on to the game, we’d be too entrenched to beat. Core to the success of the plan was one very difficult thing: survival.

In this era, the half-life of a cryptocurrency startup was about six months. Companies were dropping like flies to hacks, regulatory shutdowns, freeze-outs by banks, and rogue founders. The possibility of falling victim to one of these events was very scary. Instead of avoiding our fear, we focused on it, and forced ourselves to make it as specific as possible.

The resource we had that we needed to protect were the company assets — primarily investor cash. If those were lost it would be the end of the company, and potentially diminish our careers. To run this business we’d have to deploy most of that cash to vulnerable locations such as cryptocurrency exchange accounts, and at any given time much of it would be “nowhere”: in transit through the blockchain or the international wire system. The assets held in exchange accounts would also be actively traded by the automated systems which we would build, which could fail in any number of ways due to human or machine error.

We put all of these fears into a threat model. A simple version of it would have looked like this:

Exchange failures

- Exchange founders go rogue and steal our money

- Exchange gets hacked and hackers steal our money

- Exchange gets shut down by authorities and funds are frozen

Directed Attacks

- Our trading servers are hacked

- Our laptops or phones are hacked or stolen

- Founder is kidnapped/mugged and forced to hand over the keys

System Failures

- A bug in a trading strategy makes a bunch of bad trades and loses all our money (e.g. Knight Capital)

- A bug in our accounting logic causes our p&l numbers to be inaccurate, and lose money while we think we’re making money

Market Risks

- The price swings rapidly while we’re in a big opposite position

- Huge price drop causes company inventory to lose value

In short, we were about to run a marathon through a mine-field.

It was clear that we’d have to get really good at thinking about risk if were to have any chance at this. Almost all of this was new to us: we’d had course-work in computer security, and I was tangential to the security team while I was at Facebook, but none of us had ever thought about price risk, handling real money with algorithms, or operating in an environment in which you are constantly under attack.

Taleb’s work is expansive, but if we take only the most immediately relevant bits we might come up with a quick summary:

In any domain that contains extreme events, it is a mistake to bank your survival on your ability to precisely predict and avoid those events. Our knowledge of the world is imperfect, and there will always be an extreme case that is not in the historical data.

Rather, we should focus our attention on the impact such events would have were they to happen, and structure our systems such that they can survive, absorb, and even grow in their presence.

Applying this to our situation, we decided that the only way we could build this company was if we were willing to get hit, possibly hard, possibly often. We’d be smart and try to cut down the number of extreme events we were exposed too, but we wouldn’t put any money on our ability to avoid them. In fact the opposite: we would expect the bad thing to happen, and for each threat under consideration, we’d focus on making sure could survive the blow when it came. If we’d had a mantra it would have been this:

Expect the worst to happen. Plan how to survive it.

From this idea flowed hundreds of decisions about how to run the business, from how we chose what strategies to run, to how we set up our monitoring systems, to how we set up our information security. The starting point for how to approach any risk in our company was the assumption that our worst fears would come true.

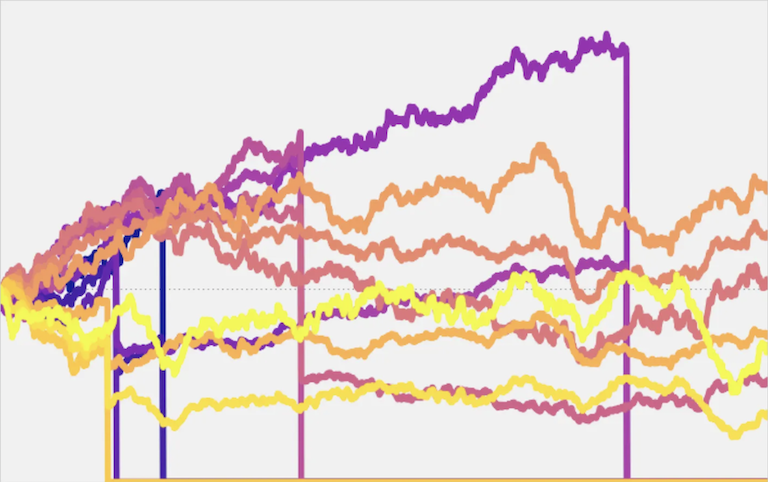

So here’s the gotcha line: we were right. Of all those things in the threat model, a lot of them really did happen, including four exchange failures and one critical trading bug (none of our machines were ever compromised). But none of those moments were fatal, in fact, the worst caused a loss of 4%. We made it through the minefield bruised but undefeated.

Here are two stories about specific threats we faced and how we survived when disaster struck.

Case Study I: The day a bug almost gave away all our money

One night in 2015, I was winding-down watching Buffy the Vampire Slayer at about 2am. My phone buzzed and I glanced over to see the home screen covered in PagerDuty alerts — I was on call that week. I got over to my desk quickly and saw that we were bleeding money at a disturbing rate: about 0.1% per minute. We’d be down 10% by the end of the hour. It was instantly clear that this was the worst trading error we had ever encountered, and if we didn’t stop it the company would be dead by the morning.

Of course, that didn’t happen. As soon as I understood the effect, I shut down all trading, closed our open positions, and began to survey the damage and diagnose the issue. We had lost a total of 0.3%. The next day, we discovered that the cause of the issue was a bizarre interaction between one of our redundancy systems and unexpected time-out behaviour from one particular exchange. It was a complex set of interactions that could not have been predicted ahead of time. We fixed the issue and were trading full-bore again by the end of the day.

There are two reasons why we survived that day and did not become a mini-Knight Capital. The proximate cause was that we had obsessive, redundant, default-fail monitoring of every aspect of our trading systems. The issue that occurred was detected by three different monitoring processes on two different machines. If my phone had been dead or I otherwise wasn’t able to catch the issue, within five minutes one of my colleague’s phones would have been jumping off the nightstand.

But the ultimate cause that we woke up that day down 0.3% and not 20% is that we expected that one day we would push a critical trading bug into production. Expect the worst to happen. Plan how to survive it. We knew that we were fallible, and that engineers with far more experience than us had blown up their companies with such errors. We didn’t know how or when, but we knew there were things we could do to minimize the damage when it happened: catch it early, have redundancies, have simple kill-switches ready. In the end, this was a scary moment but it wasn’t a near miss. We were just prepared.

Case Study II: Trusting people you don’t trust

Of any of the items in that threat-model above, the one that kept us awake at night was the fear that an exchange would blow up while we had a pile of cash sitting with them. Exchanges were dropping like flies at the time. Mt. Gox exploded in 2014. BTC-E, one of the biggest exchanges of the day, was likely run by the Russian underworld. In order to do the trading that we wanted to do, we had to hand off almost all of our funds to organizations like this.

So we went back to first principles and figured out how to survive. There were two approaches to the problem of exchange failures, whatever their cause: try to avoid them, and try to survive them.

Avoiding failures meant predicting them, and we already knew we couldn’t do this precisely (which exchanges will fail at what times). What we could do was make some negative bets: “this exchange is likely to fail sometime in some way” and avoid those exchanges altogether. To do this we came up with a checklist of positive conditions that any exchange would have to meet in order for us to trust them with any amount of money. Most of these rules were simple and easy to check, like:

- Must have a strong relationship with a credible bank

- Must have fiat currency deposits and withdrawals

- Must have a human contact we can get on the phone within a day

- …

Some of these might seem trivial on their own, but the advantage of checklists is that they can build a high-information picture of a system with low cognitive load. Consider the number of plane crashes or operating-room mistakes that have been avoided using checklists. For our purposes this meant that whenever we started thinking about a new exchange, the question was simple: does it pass the checklist or not? You’re much less likely to make a dumb mistake answering a simple question than a complicated one. Similarly, we could regularly audit our exchange roster and boot any one which fell below the waterline.

But we weren’t going to bank our survival on avoiding exchange failures. Expect the worst to happen, plan to survive it. We still had to be prepared to survive if and when an exchange got hit while we had funds at risk.

We decided to do this by setting strict limits to how much money could be kept in each account. Working backwards from the assumption that we would get hit, the first conclusion was we could never have a single point of failure on our exchange roster. Even if the most trusted exchange fails with a complete loss of funds we should be able to continue operating. So we set a single global restriction, that we’d never have more than x% of our assets in any account, and set x such that the loss would hurt bad, but we could survive.

Then we went through each exchange individually and set an even more restrictive limit based on any extra information that wasn’t already captured in our trust checklist. Sometimes this was something specific, sometimes it was semi-inside information (the crypto world was small at the time), and other times it was just our own intuition.

It was always tempting to break these limits. Every day there was some profit somewhere that we weren’t taking, only because we refused to risk more assets on that exchange. But we stuck to our account limits religiously, because that was the only way this worked. Fraud often looks like opportunity, and many of those temptations were traps of one kind or another. If we compromised enough times based on short-term emotions, we knew we’d eventually find ourselves caught out with paper profits on a dead exchange.

After all of this thinking and worrying over five years, Tinker survived four major exchange hacks and one rogue exchange founder while we had funds at risk. Five other exchanges (not in the previous list) ceased operations while we were working with them, some in an orderly wind-down, and others less so. In most of these cases Tinker ultimately accrued no loss, the largest single loss from any of these events was 4%, and the total of all losses was under 6% (about 1.1% annualized). It’s impossible to quantify the number of failures we simply avoided, but it’s likely in the dozens.

Details < Approach < Understanding

I’m sure I have four or five other case-studies I could turn into posts of their own. The details are interesting because they seem to be the answer to the title “How we survived five years in the most dangerous market in the world” As I’ve hammered home already, the reason we got the details right was because we had the right approach. Expect the worst to happen. Plan to survive it.

But the reason we had the right approach was that we built a good understanding of the role that risk played in our business. I use the word “built” instead of “had”, because it was an effortful process, not a static piece of knowledge that we entered the project with. We built that understanding starting with brutal honesty about the ways things could go wrong. For each of these risks we thought hard about the characteristics, quickly realizing that we were in a domain where extreme events were the norm, and that these could not be modelled, predicted, or reliably avoided. We understood that we ourselves were a source of risk, through human fallibility or impulsiveness. And we knew that for our purposes, survival was the most critical focus.

Finally, for all this talk of hazards and catastrophes, I’ve ignored one of the core parts of that understanding: that risk was good, in fact it was reason to take on the project in the first place. The risk in these markets shooed competitors away like a bug lamp, and created an opportunity to build an early lead. You couldn’t have the project without the risk, and the risk was why the project was worth doing. My best wishes for you, reader, are that you you find many risks worth taking, and understand them well.

The goal of Tinker was to build the Goldman Sachs of the blockchain-future, and our thesis was good. Granting that cryptocurrencies would be the next medium of finance, we’d start out with an early lead in market making, use that edge to expand into other investment products as the market grew, and by the time the traditional investment banks caught on to the game, we’d be too entrenched to beat. Core to the success of the plan was one very difficult thing: survival.

In this era, the half-life of a cryptocurrency startup was about six months. Companies were dropping like flies to hacks, regulatory shutdowns, freeze-outs by banks, and rogue founders. The possibility of falling victim to one of these events was very scary. Instead of avoiding our fear, we focused on it, and forced ourselves to make it as specific as possible.

The resource we had that we needed to protect were the company assets — primarily investor cash. If those were lost it would be the end of the company, and potentially diminish our careers. To run this business we’d have to deploy most of that cash to vulnerable locations such as cryptocurrency exchange accounts, and at any given time much of it would be “nowhere”: in transit through the blockchain or the international wire system. The assets held in exchange accounts would also be actively traded by the automated systems which we would build, which could fail in any number of ways due to human or machine error.

We put all of these fears into a threat model. A simple version of it would have looked like this:

Exchange failures

- Exchange founders go rogue and steal our money

- Exchange gets hacked and hackers steal our money

- Exchange gets shut down by authorities and funds are frozen

Directed Attacks

- Our trading servers are hacked

- Our laptops or phones are hacked or stolen

- Founder is kidnapped/mugged and forced to hand over the keys

System Failures

- A bug in a trading strategy makes a bunch of bad trades and loses all our money (e.g. Knight Capital)

- A bug in our accounting logic causes our p&l numbers to be inaccurate, and lose money while we think we’re making money

Market Risks

- The price swings rapidly while we’re in a big opposite position

- Huge price drop causes company inventory to lose value

In short, we were about to run a marathon through a mine-field.

It was clear that we’d have to get really good at thinking about risk if were to have any chance at this. Almost all of this was new to us: we’d had course-work in computer security, and I was tangential to the security team while I was at Facebook, but none of us had ever thought about price risk, handling real money with algorithms, or operating in an environment in which you are constantly under attack.

Taleb’s work is expansive, but if we take only the most immediately relevant bits we might come up with a quick summary:

In any domain that contains extreme events, it is a mistake to bank your survival on your ability to precisely predict and avoid those events. Our knowledge of the world is imperfect, and there will always be an extreme case that is not in the historical data.

Rather, we should focus our attention on the impact such events would have were they to happen, and structure our systems such that they can survive, absorb, and even grow in their presence.

Applying this to our situation, we decided that the only way we could build this company was if we were willing to get hit, possibly hard, possibly often. We’d be smart and try to cut down the number of extreme events we were exposed too, but we wouldn’t put any money on our ability to avoid them. In fact the opposite: we would expect the bad thing to happen, and for each threat under consideration, we’d focus on making sure could survive the blow when it came. If we’d had a mantra it would have been this:

Expect the worst to happen. Plan how to survive it.

From this idea flowed hundreds of decisions about how to run the business, from how we chose what strategies to run, to how we set up our monitoring systems, to how we set up our information security. The starting point for how to approach any risk in our company was the assumption that our worst fears would come true.

So here’s the gotcha line: we were right. Of all those things in the threat model, a lot of them really did happen, including four exchange failures and one critical trading bug (none of our machines were ever compromised). But none of those moments were fatal, in fact, the worst caused a loss of 4%. We made it through the minefield bruised but undefeated.

Here are two stories about specific threats we faced and how we survived when disaster struck.

Case Study I: The day a bug almost gave away all our money

One night in 2015, I was winding-down watching Buffy the Vampire Slayer at about 2am. My phone buzzed and I glanced over to see the home screen covered in PagerDuty alerts — I was on call that week. I got over to my desk quickly and saw that we were bleeding money at a disturbing rate: about 0.1% per minute. We’d be down 10% by the end of the hour. It was instantly clear that this was the worst trading error we had ever encountered, and if we didn’t stop it the company would be dead by the morning.

Of course, that didn’t happen. As soon as I understood the effect, I shut down all trading, closed our open positions, and began to survey the damage and diagnose the issue. We had lost a total of 0.3%. The next day, we discovered that the cause of the issue was a bizarre interaction between one of our redundancy systems and unexpected time-out behaviour from one particular exchange. It was a complex set of interactions that could not have been predicted ahead of time. We fixed the issue and were trading full-bore again by the end of the day.

There are two reasons why we survived that day and did not become a mini-Knight Capital. The proximate cause was that we had obsessive, redundant, default-fail monitoring of every aspect of our trading systems. The issue that occurred was detected by three different monitoring processes on two different machines. If my phone had been dead or I otherwise wasn’t able to catch the issue, within five minutes one of my colleague’s phones would have been jumping off the nightstand.

But the ultimate cause that we woke up that day down 0.3% and not 20% is that we expected that one day we would push a critical trading bug into production. Expect the worst to happen. Plan how to survive it. We knew that we were fallible, and that engineers with far more experience than us had blown up their companies with such errors. We didn’t know how or when, but we knew there were things we could do to minimize the damage when it happened: catch it early, have redundancies, have simple kill-switches ready. In the end, this was a scary moment but it wasn’t a near miss. We were just prepared.

Case Study II: Trusting people you don’t trust

Of any of the items in that threat-model above, the one that kept us awake at night was the fear that an exchange would blow up while we had a pile of cash sitting with them. Exchanges were dropping like flies at the time. Mt. Gox exploded in 2014. BTC-E, one of the biggest exchanges of the day, was likely run by the Russian underworld. In order to do the trading that we wanted to do, we had to hand off almost all of our funds to organizations like this.

So we went back to first principles and figured out how to survive. There were two approaches to the problem of exchange failures, whatever their cause: try to avoid them, and try to survive them.

Avoiding failures meant predicting them, and we already knew we couldn’t do this precisely (which exchanges will fail at what times). What we could do was make some negative bets: “this exchange is likely to fail sometime in some way” and avoid those exchanges altogether. To do this we came up with a checklist of positive conditions that any exchange would have to meet in order for us to trust them with any amount of money. Most of these rules were simple and easy to check, like:

- Must have a strong relationship with a credible bank

- Must have fiat currency deposits and withdrawals

- Must have a human contact we can get on the phone within a day

- …

Some of these might seem trivial on their own, but the advantage of checklists is that they can build a high-information picture of a system with low cognitive load. Consider the number of plane crashes or operating-room mistakes that have been avoided using checklists. For our purposes this meant that whenever we started thinking about a new exchange, the question was simple: does it pass the checklist or not? You’re much less likely to make a dumb mistake answering a simple question than a complicated one. Similarly, we could regularly audit our exchange roster and boot any one which fell below the waterline.

But we weren’t going to bank our survival on avoiding exchange failures. Expect the worst to happen, plan to survive it. We still had to be prepared to survive if and when an exchange got hit while we had funds at risk.

We decided to do this by setting strict limits to how much money could be kept in each account. Working backwards from the assumption that we would get hit, the first conclusion was we could never have a single point of failure on our exchange roster. Even if the most trusted exchange fails with a complete loss of funds we should be able to continue operating. So we set a single global restriction, that we’d never have more than x% of our assets in any account, and set x such that the loss would hurt bad, but we could survive.

Then we went through each exchange individually and set an even more restrictive limit based on any extra information that wasn’t already captured in our trust checklist. Sometimes this was something specific, sometimes it was semi-inside information (the crypto world was small at the time), and other times it was just our own intuition.

It was always tempting to break these limits. Every day there was some profit somewhere that we weren’t taking, only because we refused to risk more assets on that exchange. But we stuck to our account limits religiously, because that was the only way this worked. Fraud often looks like opportunity, and many of those temptations were traps of one kind or another. If we compromised enough times based on short-term emotions, we knew we’d eventually find ourselves caught out with paper profits on a dead exchange.

After all of this thinking and worrying over five years, Tinker survived four major exchange hacks and one rogue exchange founder while we had funds at risk. Five other exchanges (not in the previous list) ceased operations while we were working with them, some in an orderly wind-down, and others less so. In most of these cases Tinker ultimately accrued no loss, the largest single loss from any of these events was 4%, and the total of all losses was under 6% (about 1.1% annualized). It’s impossible to quantify the number of failures we simply avoided, but it’s likely in the dozens.

Details < Approach < Understanding

I’m sure I have four or five other case-studies I could turn into posts of their own. The details are interesting because they seem to be the answer to the title “How we survived five years in the most dangerous market in the world” As I’ve hammered home already, the reason we got the details right was because we had the right approach. Expect the worst to happen. Plan to survive it.

But the reason we had the right approach was that we built a good understanding of the role that risk played in our business. I use the word “built” instead of “had”, because it was an effortful process, not a static piece of knowledge that we entered the project with. We built that understanding starting with brutal honesty about the ways things could go wrong. For each of these risks we thought hard about the characteristics, quickly realizing that we were in a domain where extreme events were the norm, and that these could not be modelled, predicted, or reliably avoided. We understood that we ourselves were a source of risk, through human fallibility or impulsiveness. And we knew that for our purposes, survival was the most critical focus.

Finally, for all this talk of hazards and catastrophes, I’ve ignored one of the core parts of that understanding: that risk was good, in fact it was reason to take on the project in the first place. The risk in these markets shooed competitors away like a bug lamp, and created an opportunity to build an early lead. You couldn’t have the project without the risk, and the risk was why the project was worth doing. My best wishes for you, reader, are that you you find many risks worth taking, and understand them well.